Financing in the Fall of 2019

If you follow the housing and/or the financial markets, you’ve probably heard that the Federal Reserve reduced the Central Banks’ lending rate by 0.25% during its late July meeting. Amazingly, this was the first time that the Fed reduced its borrowing rate in 11 years and comes on the heels of 2018 when the Fed increased its rate in each of the four calendar-year meetings.

So, what does this mean for the housing market and, more specifically, the luxury market in Boston that we track very closely? Well, for starters, the fall of 2019 looks like a great time to borrow money! Mortgage rates (which do not exactly parallel the Fed lending rate) are bumping up against historical lows. So, take a hard look at your mortgage rate if you love your home (possible refi) and take a hard look at the market in the event you might be thinking about a move… this could be a good time to do so!

Don’t forget Seasonality!

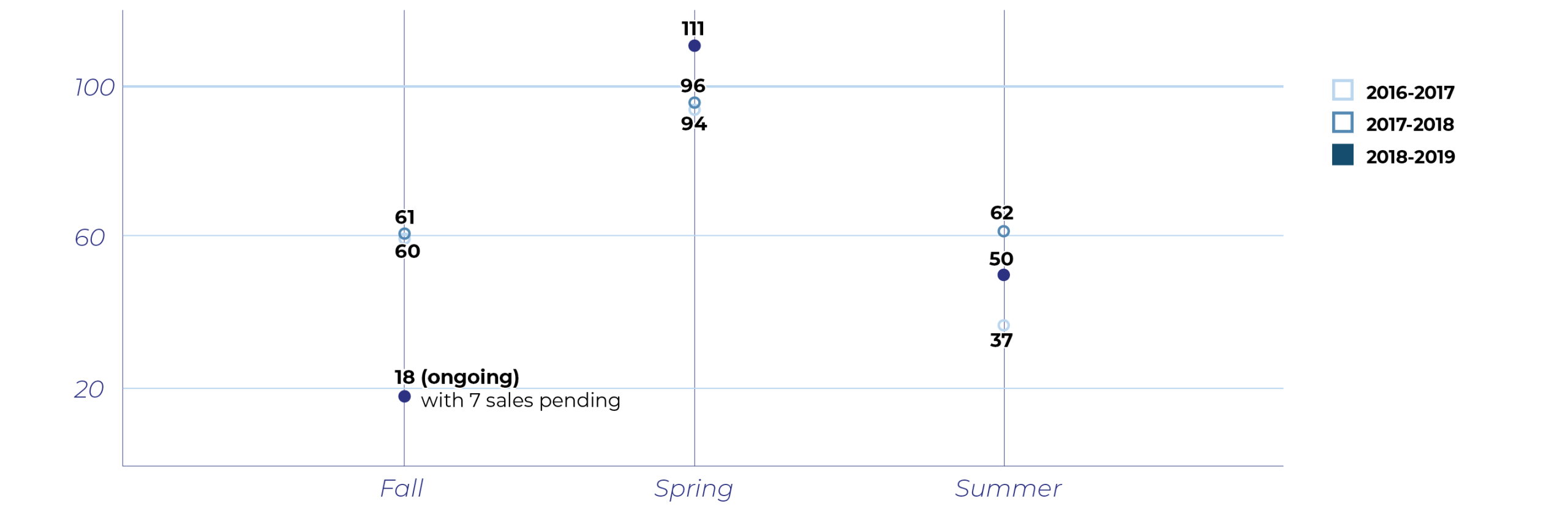

Coming out of the summer months in the Boston luxury market, we expect lower interest rates to generate a robust fall market in 2019. Admittedly, the fall is typically a slower time with less active buyers and less motivated sellers. If you haven’t seen the difference between spring and fall market activity, here it is a graphical perspective from the last three years.

Sales over $2M in Back Bay, South End and Beacon Hill

*Fall defined as sales closing between 10/15 and 1/15 each year. Spring defined as sales closing between 4/15 and 7/31 each year. Summer defined as sales closing between 8/1 and 10/14 each year. Please note that “sales activity” happens 30-60 days after buyers are “active” in the market.

Let’s get a bit more granular with a sampling of mortgage options…

Wells Fargo, a bank that has been aggressive with mortgage dollars in our Boston market in 2019, is currently offering a sub 3.5% rate on a 30 year jumbo fixed mortgage! Jumbo mortgages are loans that exceed $453,000.

Further, if a buyer is willing to suspend their disbelief that he/she might not be in the same home in 10 years (we don’t often see that longevity in the city!), they can and should opt for a 5, 7 or 10 year adjustable rate mortgage (ARM). This locks in the term of your rate for a specified number of years before adjusting (typically) upwards after that period.

As an example, locking in a 7 year ARM in 2019 would give you until 2026 to either refinance or sell the home before your rate changed. A lot can (and usually does) happen in seven years. Pets can join and depart your ranks, multiple kids/grandkids arrive, promotions emerge, jobs transition and on and on. For “risking” a shorter lock period, banks are willing to reduce the rate well below what you might receive for a fixed 30 year term. Currently, a 7 year jumbo ARM is offered at 2.625% by Wells Fargo.

If you’re a REAL risk taker and want the lowest possible monthly payment on your mortgage, let’s talk interest only loans! The mortgages previously mentioned require one to pay principal and interest each month. Don’t get us wrong, paying off principal each month is a positive thing that ultimately leads to wealth creation. However, if you have other uses for your cash and have an adequate down payment (20% or more), then acquiring an interest-only mortgage allows you to preserve capital and keep your housing costs to a minimum while steering your cash towards more compelling assets or opportunities.

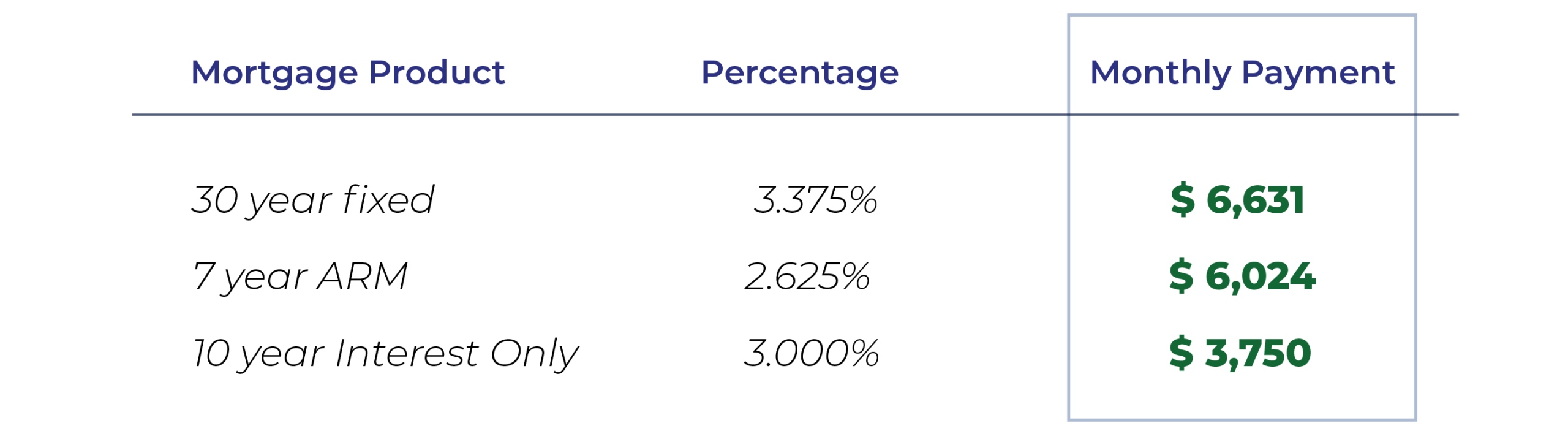

Let’s take a look at 249 Beacon St, # 2

A 2 bedrooms, 2.5 bathrooms, 1,952 square foot apartment in the Lower Back Bay.

Assuming a two million dollar purchase with a 25% down payment, here are what the payments would looks like on different mortgage products:

Keep in mind, mortgage rates are always dependent on credit and, to a degree, housing stock. Single families, condos and multifamilies may well have different rates even for the same borrower. Owner occupant rates are always cheaper than investor interest rates. Lastly, they are subject to change without much notice.