COG Mid Year Report

With the first two quarters of 2017 behind us, it is a good time to reflect on the state of the Boston luxury real estate market as we push through the

summer doldrums.

Speaking generally, we have seen increases in pricing for our primary neighborhoods in the first half of the year. Looking specifically at the absolute

price point, Back Bay saw an increase of $309,583 in Average Sale Price, a 12.3% increase from mid year 2016 to mid year 2017. Beacon Hill increased

by $942,124 in Average Sale Price, a 44% increase over the same time period.* While both of these neighborhoods increased in Average Sale Price, the

South End saw a decrease in Average Sale Price by $22,177, a 1.3% negative change year over year.

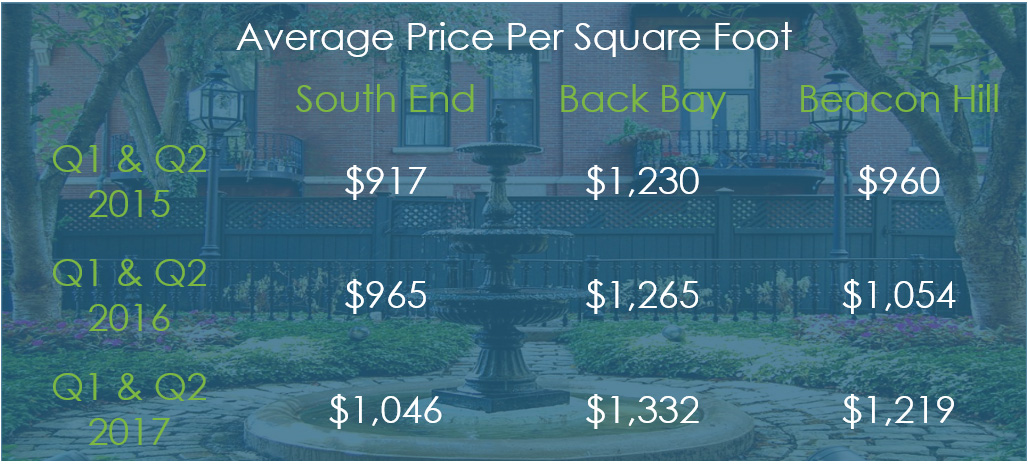

Absolute ($) pricing is always good to keep an eye on but, particularly with condominiums, we prefer price per square foot as our metric of choice when

analyzing the market’s relative strength. This metric increased significantly across all three neighborhoods: 15.7% in Beacon Hill, 5.3% in Back Bay,

and 8.4% in the South End. We typically expect that with rising sale prices, we would also see rising sale price per square foot, and vice versa. However,

in this case, we see the South End decrease in sale price and increase in price per square foot. Intuitively, we understand this to mean that people

are buying smaller houses over the first 2 quarters of 2017 when compared with the same time frame in 2016. In Q1 and Q2 of 2017 the average square

footage of a unit that sold in the South End was 1,664 SF, whereas in 2016 it was 1,798 SF. It’s hard to know why the inventory for sale has trended

smaller in the South End but that is what the data shows.

*Beacon Hill pricing increases were driven in large part by a new development at 32 Derne Street. 8 units sold in this complex in the first half of 2017

with prices ranging from $2.2M to $9M. The average price per foot across these units was $1,530. There had not been a delivery with this many new construction

units in Beacon Hill in recent history.

Delving deeper into each individual neighborhood, we have seen growth across all three of our core neighborhoods. See below for detailed statistical analysis

of the changes experienced in each.

SOUTH END

Average ($/SF) increased 5.2% from mid year 2015 to mid year 2016

Average ($/SF) increased 8.4% between mid year 2016 and mid year 2017

Overall, average price per square foot grew 14% between mid year 2015 and mid year 2017.

BACK BAY

Average ($/SF) increased 2.8% from mid year 2015 to mid year 2016,

Average ($/SF) increased 5.3%between mid year 2016 and mid year 2017.

Overall, there was an 8.3% increase in the average ($/SF) between mid year 2015 and mid year 2017.

BEACON HILL

Average ($/SF) increased 9.8% from $960 mid year 2015 to $1,054 mid year 2016.

Average ($/SF) increased 15.7% between mid year 2016 and mid year 2017.

Overall, there was a 27% increase in the average ($/SF) between mid year 2015 and mid year 2017

*Again, it is important to note that the percentage growth in Beacon Hill has been largely skewed due to the sales at The Whitwell, a new luxury condo

building located at 32 Derne Street. The units in this building traded for an average of $1,530 per SF throughout the year, approximately 32% more

than the average ($/SF), of $1,157, throughout the rest of the neighborhood.

When looking strictly at the number of sales per month in the first half of the year for the last three years (2015-2017), the seasonality of our business

remains consistent.. Empirically, we feel this to be the case as the majority of home buying and selling activity happens in early spring, typically

April and May, resulting in closings in June. Looking closely at these numbers, the South End saw 40 sales in June 2017. Compare this against the 6

month running average of 17 sales per month and you start to appreciate the tradition that is “spring selling season”. The pattern continues across

the Back Bay where there were 25 sales this June, 58% more than the average from January through June of 15. Beacon Hill also experienced its highest

number of sales in the month of June, boasting 16 sales, 100% more than the average during the first half of the year: 8.

SOUTH END AND BACK BAY AVERAGE SUPPLY – QUARTERLY

Months of supply is a measure used in real estate to predict how many months it would take for the number of homes currently on the market to sell, given

the pace at which homes are currently selling, assuming that no new listings became available. For example, if there are currently 100 homes on the

market with 20 homes selling each month, there is a 5 month supply of homes in this market. This metric is a good indicator of whether the market is

favoring buyers or sellers. If a market has less than 6 months of supply we assume that the market is more favorable to sellers. If a market has more

than 6 months of supply than this indicates that the market is more buyer friendly, due to an excess of inventory in the market.

Review the charts below to see how supply has changed over the last 6 quarters in the Back Bay and South End. In the South End, in particular, there is

evidence of a rather significant increase in supply in the $3 to $4M range. This is primarily the result of condo conversion projects that have hit

the market.

While the spring season was active and dynamic with pricing increases and sales, the summer appears to be settling into its typical slow down. It’s hard

to imagine pricing picking up in September where it left off in June. All indications are that mortgage rates will continue to climb, albeit, gradually.

As such, expect luxury condo and townhome pricing in Boston to plateau through at least the beginning of 2018.

Don’t hesitate to be in touch if you’d like to delve deeper into this data with us. We’re always happy to discuss micro neighborhoods inside our larger

market areas.