Your boutique residential real estate consultancy and brokerage specializing in Boston’s most highly sought addresses.

2022: $2M+ Sales Boston Market Overview

BY Rachel Bakish |

February 4, 2022

Well, at least the worst is behind us, right?

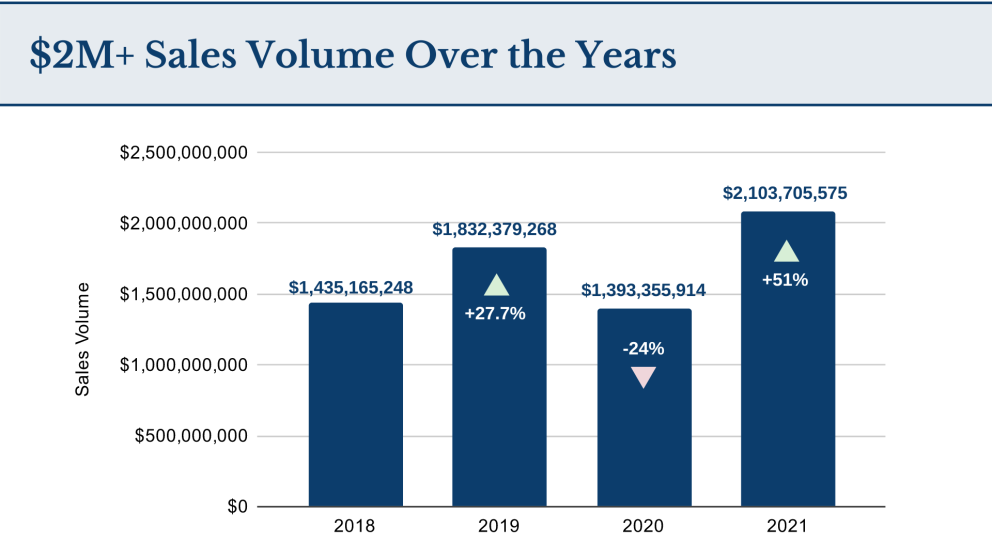

Even as the virus continued to torment city businesses and citizens with never ending regulations and protocols, the theme for 2021 was the tremendous bounce back we saw in transaction volume across our market. Whereas the city dropped off by 28% of its sale’s volume from 2019 to 2020, the year of 2021 saw a steely 51% gain in sales volume versus 2020. Even comparing the sales volume from 2021 against 2019 is impressive with the most recent year gaining nearly 14.8% total sales volume against a strong market in 2019.

To be sure, 2021 was indeed a record setter for the luxury market in the city with an amazing $2.103B in transaction volume for deals above $2M. The pricing per square foot dropped slightly in 2021 ($1,635/SF) from 2020 ($1,676/SF) but the number of transactions that were inked grew from 347 in 2020 to 529 in 2021! For context, there were 481 deals in 2019.

As has been the trend for a number of years now, the upper reaches of the luxury market continue to be defined by the new offerings in the full service category. These are the elevator and concierge style mid to high rise buildings that are interspersed around our otherwise “short,” brownstone-driven city. Notably, the only new building to come online fully in 2021 was the Sudbury, located in the Midtown market. It delivered its first 10 (of 55) units to the market in 2021 with an average selling price of $2,153/SF. Phase two of the Echelon property in the Seaport also entered the market in force in 2021 with 32 closings for more than $2M.

One Dalton delivered more new homes in 2021 (as well as some resales) contributing $106,727,418 volume to the market (5% of the market total). The pricing in this building alone continues to lift the overall average across the market by $47/SF. On the whole, this is the most expensive building in Boston.

As we work through 2022, two new buildings are garnering most of the attention and headlines for luxury and sophistication. First, the St. Regis Residences will offer 114 units to the Seaport market (likely to deliver in 2023). Second, the Raffles Hotel and Residences development in Back Bay (Prudential) will deliver 146 units to the luxury market in late 2022 or early 2023. Sales in both of these buildings appear to be strong as we write in early 2022. At this point, one can expect the new, high-rise buildings around the city to command pricing of at least $2,500/ SF with the top units approaching and exceeding $4,000/SF.

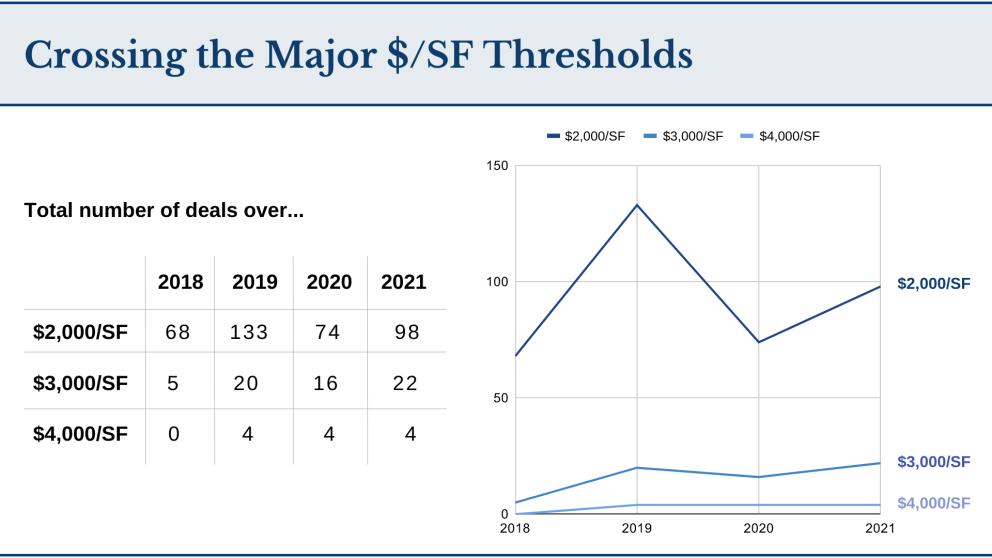

In 2018 when we wrote this report we were tracking the total number of deals over $2,000/SF in the market as well as the deals over $3,000/SF and $4,000/SF. As of 2021, there are 98 deals over $2,000/SF and that threshold no longer seems like a barrier to the ultra luxury homes in the city. See the graph below to understand how the luxury market has grown.

Even the brownstone category has gotten in on the $3,000+ per square foot category. In 2021, 29 Commonwealth Ave unveiled 9 new units to the market. Bostonians will recognize this address as the tallest of the row houses in Back Bay. It sits on the corner of Comm and Berkeley Street towering over its surrounding peers. Five of the nine units closed in 2021 with average pricing of $3,320/SF!

Of the six broader markets that we track, Beacon Hill, Back Bay and the Waterfront had lower average prices per foot in 2021 than they did in 2020. Meanwhile, South End, Seaport and Midtown were all up in pricing in 2021. As was the trend across the entire market, the volume and transaction count in Seaport were both up significantly this year (70% increase in volume; 40% increase in number of transactions) as more and more inventory enters that market.

Looking ahead

We’re expecting big things from the market in 2022. For starters, our underlying assumption is that the Black Swan Coronavirus will finally sing its swan song and make a meaningful exit from the headlines this year. As such, we expect city real estate to prosper. There’s very little getting around our major impediment in this market: a lack of inventory. Regulation around development here, not to mention sky-high construction pricing, continues to place strict limitations on the number of new units that can serve our growing population (approx. 675,000 in the 2020 census – up 9.4% from 2010!).

Without vast increases in the number of units that can serve a growing population (manifesting itself as robust housing demand), there’s simply one directionthat the pricing can go. On top of the supply shortage, the headlines continue to extoll the most significant inflation in the nation in 40 years. In early 2022, the rumors from the Fed are that their rates will definitely rise throughout this year. With increasing interest rates we might expect to see pricing in the market dip. However, that pesky demand side, particularly in the high end of the market, is likely to be unwavering in the face of rising rates… at least for this year!

Our spring sales market, defined as March through June, almost always sets the tone for the year. Larger corporations, which have largely embraced Work from Home for two years, are likely to bring workers back (or at least announce returns) in time for the spring market. Such movement from these companies should have cascading effects with both young professionals and empty nesters as they look to solidify their housing situation in the city believing that the virus is behind us for good. With the consumer (buyer) interest that we witnessed across our listings in the fall of 2021, we are expecting nothing short of one of the strongest spring housing markets we’ve seen in the Boston luxury markets in 2022.

Looking For More, Read our Full Report >